Auto-populated Delta Hedge Quantity

Auto-populated Delta Hedge Quantity

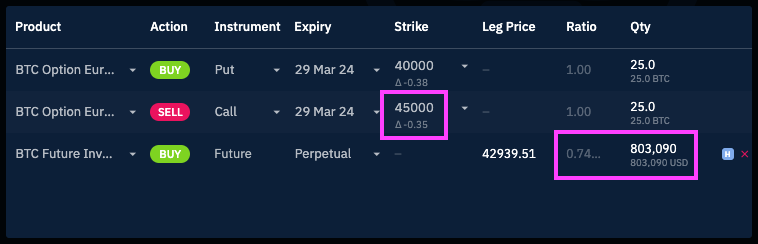

Starting 1 February 2024, we will automatically calculate and fill in the Quantity when you add a hedge leg to your Options structure.

How is the Delta Hedge Quantity Calculated?

The calculation uses the respective venue’s live market data, including Options Delta, Mark Price, and the Underlying Futures Price.

Specifics for Deribit:

For options on Deribit, which are inverse-margined and have premiums in the base currency, the premium-adjusted delta is used for calculating the quantity.

Specifics for Bybit and BIT:

For venues that have linear-margined options and have premiums in the alternate currency, delta is used for calculating the quantity.

Dynamic Recalculation

The hedge quantity will automatically recalculate whenever there are changes to the Options Structure’s details. This includes modifications to the options legs or changes in the underlying futures price.

This automatic recalculation ensures the hedge quantity remains closely aligned with market expectations. It also allows you to verify if your intended input is close to the system’s pre-calculated values.

Important for Custom Quantities:

If you prefer to set a custom quantity for your delta hedge, you should:

- Firstly, adjust your options strategy details and the price of the hedge leg.

- Then, as the final step, enter your custom hedge quantity.